The Environmental Omnibus Proposal

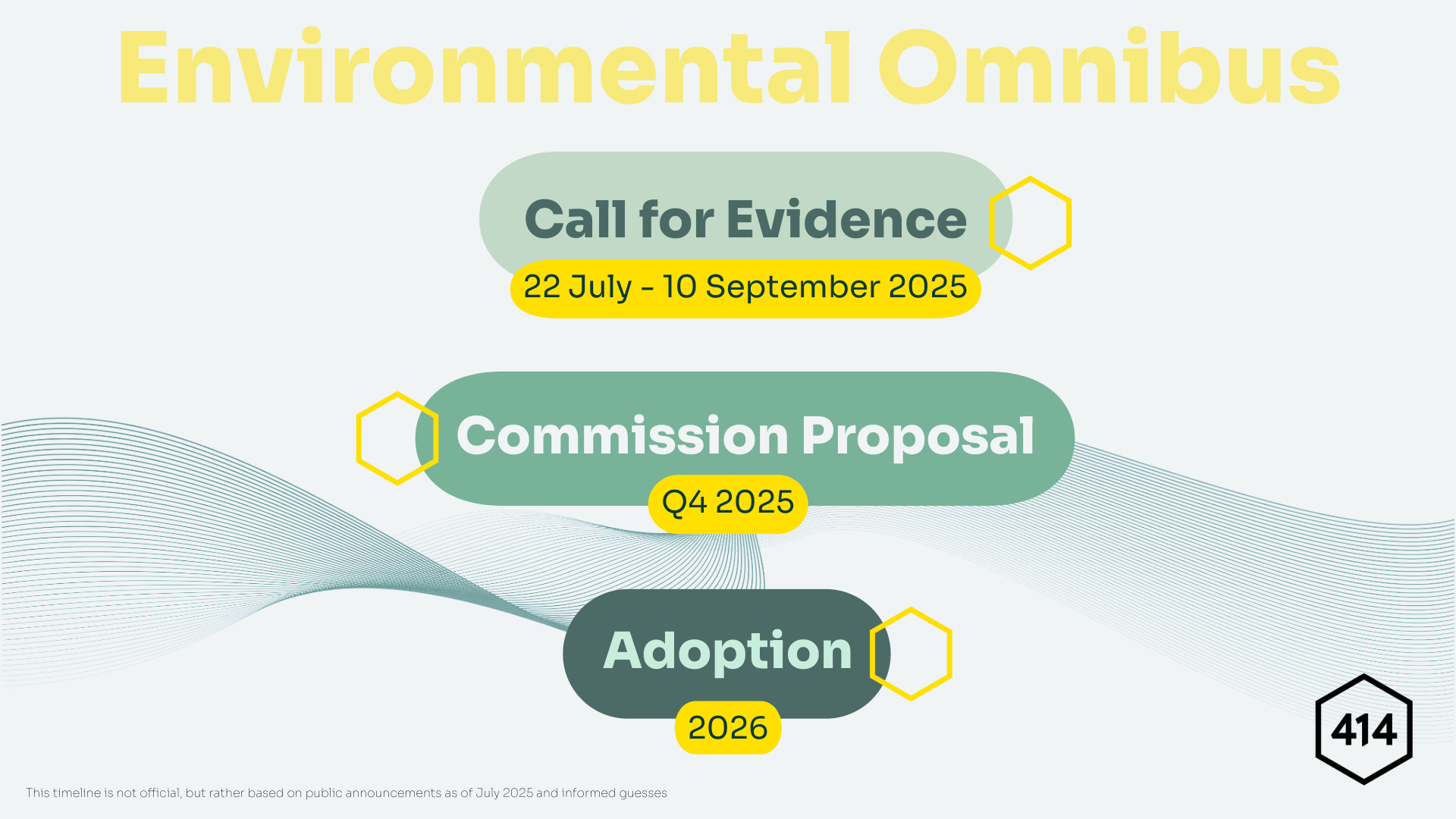

The European Commission has launched a Call for Evidence to identify opportunities to simplify and streamline EU environmental legislation. This move is part of a broader “Environmental Omnibus Proposal”, which aims to reduce administrative burdens for businesses operating under circular economy, waste, and industrial emissions rules.

Just a few months ago we saw the first Omnibus Package come out on Sustainability Reporting, amending the CSRD, CSDDD and EU Taxonomy, and stripping them of 80% of their regulatory burden (as well as of their effectiveness).

The Commission’s objective is to make implementation of environmental law faster, easier, and more cost-effective, particularly for small and medium-sized enterprises. The proposed measures range from eliminating duplicative reporting to accelerating permitting and digitalising compliance processes.

While not directly targeting financial entities, these changes may have notable implications for private market investors, particularly those with exposure to industrial, construction or consumer goods.

Who’s Affected?

The call for evidence does not specify which existing environmental laws may be simplified. Instead, it highlights a few potential policy areas for inclusion in the upcoming Environmental Omnibus, while noting that the final scope will depend on the feedback gathered through the consultation process.

The initiative is primarily aimed at operators and producers subject to environmental compliance requirements.The areas under review include:

- Extended Producer Responsibility (EPR) for products like electronics, packaging, and batteries.

- Waste management regulations, particularly those involving hazardous substances.

- Industrial installations subject to permitting and emissions controls.

- Construction and demolition firms handling regulated materials.

For general partners and investors with exposure to these sectors, it’s worth assessing how simplification efforts may alter compliance landscapes for better or worse.

Amendments to the Waste Framework Directive (WFD)

The SCIP database, introduced under the WFD, requires companies to report when their products contain substances of very high concern, such as carcinogens or persistent pollutants. The Commission is considering its removal to reduce administrative load.

SCIP stands for Substances of Concern In Products and applies across supply chains involving electronics, building materials, automotive components and chemicals. Without it, access to information on hazardous content may become more limited particularly for recyclers or waste processors.

.png)

While reduced reporting obligations may lower compliance costs, some operators may find it more difficult to conduct internal risk assessments or assure downstream safety practices.

This could affect both operational efficiency and ESG transparency, particularly where end-of-life product handling is involved.

Streamlined Extended Producer Responsibility (EPR) Rules

The proposal also considers harmonising and simplifying EPR obligations across EU member states, especially for producers selling into multiple markets.

EPR applies to producers of packaging, electronics, batteries, textiles and other regulated products. For firms active across jurisdictions, streamlined rules may ease administrative friction.

However, depending on how “facilitation” is implemented, the stringency of reporting or accountability could shift. Some industry stakeholders have noted that EPR-related safety and design standards, such as for lithium-ion batteries, are essential to prevent incidents during waste handling.

Faster Permitting and Less Redundancy

Another potential area of focus is the acceleration of permitting processes, alongside a reduction in “double reporting” requirements, particularly in industrial emissions and waste operations. The Commission will base the proposed amendments in its experience with the Net Zero Industry Act.

Sectors such as manufacturing, resource processing, and construction may benefit from faster project timelines and reduced regulatory overlap.

As always, speed and simplification need to be balanced with appropriate safeguards, in particular, making sure that there are still minimum environmental or occupational health standards.

Practical Consequences of Regulatory Simplification on Sustainability

The reforms tie into the EU’s Competitiveness Compass target of reducing administrative burdens by 25% across the board, and by 35% for SMEs, by 2029. For businesses navigating multi-layered environmental compliance regimes, greater clarity and efficiency are clearly welcome.

At the same time, environmental regulations often serve as a framework for operational risk identification, especially where health, safety, and material traceability are concerned.

In the absence of certain obligations, such as publicly disclosing data, companies may need to strengthen internal controls and information systems to maintain risk visibility and respond to stakeholder expectations around sustainability and safety.

Key points of discussion

Although the Commission’s proposals aim to reduce costs and improve clarity, investors may wish to consider how portfolio companies will maintain transparency, manage risk, and respond to changes in data availability or enforcement dynamics.

Key questions to reflect on:

- Are companies likely to benefit from reduced administrative complexity or could they face gaps in information needed for safe operations?

- Internal risk management systems rely on external data sources (e.g. SCIP) that might no longer be available.

- Could looser regulatory frameworks introduce latent liabilities or increase ESG performance disparities across the market?

From a portfolio management perspective, maintaining high internal standards may be a strategic choice, especially in sectors with material environmental or occupational safety exposure. The absence of regulatory obligations does not necessarily insulate companies from operational incidents or reputational scrutiny.

Next Steps

The Call for Evidence is open until 10 September 2025. Stakeholders are encouraged to contribute via the Have Your Say portal, particularly those active in relevant sectors or advising companies on compliance.

While regulatory efficiency can benefit business agility, investors may wish to encourage their portfolio companies to remain proactive in managing environmental and safety risks, even in a lighter compliance environment.

Final remarks

Lastly, we must note that one thing that stands out in the Commission’s approach is the decision not to carryout a new impact assessment. As warned in previous articles, the Commission has skipped this step in the two last Omnibus released, which has already drawn criticism. In fact, the European Ombudsman has launched a procedure questioning whether the Commission is acting within legal boundaries by rushing and skipping important parts of the legislative process.

The Commission argues that because the regulations targeted for simplification are based on relatively recent impact assessments, there’s no need to revisit them. But once again, that raises an important question: if those assessments were thorough enough to justify the original requirements as necessary and proportionate, how can the same evidence now support removing or weakening those same rules without a similarly detailed analysis?

It’s hard to see how meaningful simplification can happen without first carefully assessing how the proposed changes might affect outcomes, and whether they’re really fit for purpose in today’s context.

.png)

.png)